William E. Taylor Division is a 501(c)(3) non-profit public charity organization

The William E. Taylor Division truly appreciates and relies on the generous ongoing support we receive from sponsors both financially and materially, including military and law enforcement organizations, businesses and individuals. As our unit grows, so do our financial needs – it’s all for our cadets! Thank you.

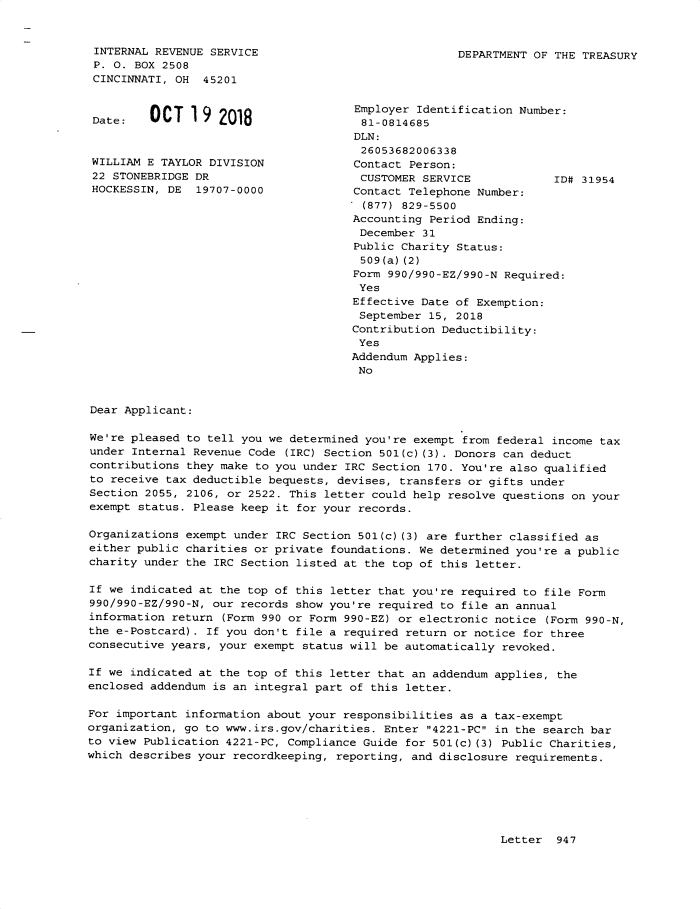

IRS Determination Letter

“William E Taylor Division” (EIN: 81-0814685)

Note: for searches on the IRS.gov site, it must be E without a period: “William E Taylor” – otherwise it fails to show our result page.

Determination Letter – A favorable determination letter is issued by the IRS when an organization meets the requirements for tax-exempt status under the Code section the organization applied.

William E Taylor Division’s IRS 501(c)(3) Determination Letter is available online at the IRS at the following link:

https://apps.irs.gov/pub/epostcard/dl/FinalLetter_81-0814685_WILLIAMETAYLORDIVISION_10042018.tif

William E Taylor Division’s IRS 501(c)(3) Determination Letter is available online at the IRS at the following link:

https://apps.irs.gov/pub/epostcard/dl/FinalLetter_81-0814685_WILLIAMETAYLORDIVISION_10042018.tif

Publication 78 Data – Organizations eligible to receive tax-deductible charitable contributions. Users may rely on this list in determining deductibility of their contributions.

On Publication 78 Data List: Yes

Deductibility Code: PC

On Publication 78 Data List: Yes

Deductibility Code: PC

In general, an individual who itemizes deductions may deduct contributions to most charitable organizations up to 50% (60% for cash contributions) of his or her adjusted gross income computed without regard to net operating loss carrybacks.

Code: PC

Type of organization and use of contribution: A public charity.

Deductibility Limitation: 50% (60% for cash contributions)

Contributions must actually be paid in cash or other property before the close of an individual’s tax year to be deductible for that tax year, whether the individual uses the cash or accrual method.

If an individual donates property other than cash to a qualified organization, the individual may generally deduct the fair market value of the property. If the property has appreciated in value, however, some adjustments may have to be made.

The rules relating to how to determine fair market value are discussed in Publication 561, Determining the Value of Donated Property. For a more comprehensive discussion of the rules covering income tax deductions for charitable contributions by individuals, see Publication 526, Charitable Contributions.